.jpg)

You Deserve a Home Upgrade

Flexible financing with no closing costs*

Your home has grown in value — now let it work for you.

At CVNB, we’re here to help you put that equity to good use. Whether you’re planning a kitchen remodel, paying off high-interest debt, sending a child to college, or taking that dream vacation, we offer flexible home equity solutions with no closing costs* when you have a CVNB checking account.

Explore Two Smart Ways to Fund What Matters Most:

-

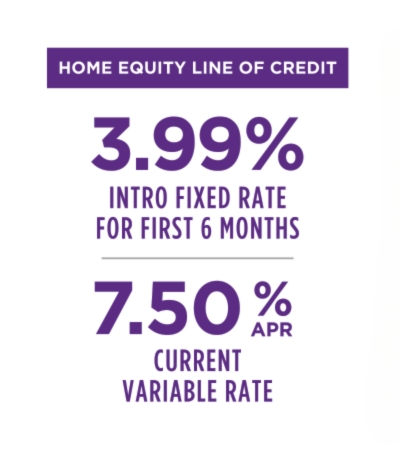

Home Equity Line of Credit (HELOC)

-

Home Equity Amortizing Loan (Second Mortgage)

Home Equity Line of Credit (HELOC)

Best for: Ongoing projects or expenses like home renovations, education costs, medical bills or paying off higher-interest debt.

- Intro Rate: 3.99% fixed APR for the first 6 months

- After the introductory period: variable APR based on the Wall Street Journal Prime Rate (7.50% as of 8/1/2025) plus a margin from -0.25% to 1.00%

- No closing costs when you have (or open) a CVNB primary checking account*

- 10-year term

- Monthly payments: 1% of the outstanding balance

- Loan amounts up to $150,000 qualify for no closing costs*

- Max Loan-to-Value (LTV): 85%

- Annual fee: $25 after the first year

- Prepayment penalty: $200 if closed within the first 3 years

- Late fee: 5% of the payment due or $25, whichever is greater

- Primary residence only

*See disclosure below for details on checking account and loan amount requirements.

.jpg)

Home Equity Amortizing Loan (Second Mortgage)

Best for: Large one-time expenses like home improvements, debt consolidation, or major purchases where you want predictable payments for the first five years.

This is a second mortgage loan where you receive funds upfront and make regular monthly payments. The rate stays the same for the first 60 months, then adjusts annually based on the 5-Year U.S. Treasury Rate.

- Intro Rate: 6.99% fixed APR for the first 60 months

- After the fixed period: Variable APR based on the 5-Year U.S. Treasury + 4.5% margin (7.72% APR as of 8/1/2025)

- No closing costs when you have (or open) a CVNB primary checking account*

- Rate caps: Max 2% per adjustment, 6% lifetime cap

- Loan amounts up to $150,000 qualify for no closing costs*

- Max Loan-to-Value (LTV): 85%

- Fully amortizing monthly payments

- Maximum term: 20 years

- Late fee: 5% of the payment due or $25, whichever is greater

- Primary residences only

*See disclosure below for details on checking account and loan amount requirements.

About the CVNB Primary Checking Account Requirement

To qualify for the no closing cost offer, the borrower must already have their primary checking account at CVNB or agree to open a primary checking account at CVNB.

A checking account is a CVNB Cumberland Checking account (Basic, Plus, or Signature) used for routine money management. The primary account must be actively used for everyday banking, including receiving direct deposits, paying bills, and using the debit card on a regular basis.

A checking account is a CVNB Cumberland Checking account (Basic, Plus, or Signature) used for routine money management. The primary account must be actively used for everyday banking, including receiving direct deposits, paying bills, and using the debit card on a regular basis.

Explore Cumberland Checking Accounts

Why Choose CVNB for Your Home Equity Loan?

-

No closing costs when you have (or open) a CVNB primary checking account*

-

Apply online when it’s convenient for you

-

We care about helping you succeed, from application to closing and beyond

-

Discover how it feels to bank with a team that truly cares

Ready to Get Started?

- Choose your loan: HELOC or Amortizing Second Mortgage

-

Apply online or visit your local branch

-

Put your equity to work on what matters most, from home upgrades to financial peace of mind

Important Disclosure Information:

Home Equity Line of Credit (HELOC): Loan amounts range from $20,000 to $150,000 with a 10-year term and a maximum Loan-to-Value (LTV) of 85%. The introductory APR is 3.99% fixed for the first six (6) months. After the introductory period, the APR becomes variable and adjusts based on the Wall Street Journal Prime Rate plus a margin ranging from -0.25% to 1.00%, depending on creditworthiness and LTV. As of August 1, 2025, the Prime Rate is 7.50%. The maximum APR is 18%. A minimum monthly payment of 1% of the outstanding balance is required. No closing costs apply for loan amounts up to $150,000 when the borrower has (or agrees to open) a CVNB primary checking account. A checking account is a CVNB Cumberland Checking account (Basic, Plus, or Signature) used for routine money management. The primary account must be actively used for everyday banking, including receiving direct deposits, paying bills, and using the debit card on a regular basis. If the loan amount exceeds $150,000, the borrower is responsible for all title work and title insurance costs. A $25 annual fee applies after the first year. A prepayment penalty of $200 applies if the HELOC is paid off and closed within the first three (3) years. A late payment fee of 5% of the payment due or $25, whichever is greater, applies to payments more than 10 days past due. Property must be the borrower's primary residence.

Home Equity Amortizing Loan (Second Mortgage): Loan amounts range from $20,000 to $150,000 with a maximum LTV of 85%. The introductory APR is 6.99% fixed for the first sixty (60) months. After the initial period, the APR becomes variable and adjusts annually based on the 5-Year U.S. Treasury Rate plus a margin of 4.5%. As of August 1, 2025, the APR is 7.72%. For Example: On a $100,000.00, 20 year ARM, the initial monthly payment for the first five years would be $774.71. The payment would then adjust based on the 5-Year U.S. Treasury Rate plus the margin. The maximum rate adjustment is 2% per adjustment, with a 6% lifetime cap. All loans are fully amortizing with regular monthly payments. No closing costs apply for loan amounts up to $150,000 when the borrower has (or agrees to open) a CVNB primary checking account. A checking account is a CVNB Cumberland Checking account (Basic, Plus, or Signature) used for routine money management. The primary account must be actively used for everyday banking, including receiving direct deposits, paying bills, and using the debit card on a regular basis. If the loan amount exceeds $150,000, the borrower is responsible for all title work and title insurance costs. A late payment fee of 5% of the payment due or $25, whichever is greater, applies to payments more than 10 days past due. This loan is available for primary residences only and is not available for second homes, investment properties, or commercial properties.

All loans are subject to credit approval, income verification, LTV requirements, and standard underwriting guidelines. Additional fees and restrictions may apply. Offer valid for a limited time and may be discontinued at any time without notice.